Taxes NY is a topic that affects every resident of the Empire State, yet many find it complex and overwhelming. Whether you're a newcomer or a long-time resident, navigating the state's tax system can be a daunting task. From income taxes to sales taxes, New York imposes a variety of levies that impact individuals and businesses alike. In this article, we will delve into the intricacies of Taxes NY, providing you with a clear understanding of how they work, what you need to know, and how to stay compliant. With the right knowledge and resources, you can make informed decisions and avoid costly mistakes.

Understanding Taxes NY requires familiarity with its various components, such as state income tax rates, property taxes, and excise taxes. Each of these plays a crucial role in funding essential public services like education, infrastructure, and healthcare. However, the complexity arises from the numerous deductions, credits, and exemptions available, which can significantly affect your tax liability. As a resident, it's important to stay updated on any changes in tax laws and regulations, as they can have a direct impact on your financial situation.

To help you navigate the world of Taxes NY, this article will explore key aspects of the state's tax system, including how to file your taxes, what deductions and credits are available, and strategies for minimizing your tax burden. Whether you're a homeowner, small business owner, or employee, the information provided here will empower you to take control of your tax obligations and ensure you're maximizing your financial potential. Let's dive into the details and uncover everything you need to know about Taxes NY.

Read also:Isaiah Evans

What Are the Key Components of Taxes NY?

Taxes NY encompasses a wide range of levies that contribute to the state's revenue. Understanding these components is essential for anyone looking to manage their finances effectively. The primary taxes include state income tax, property tax, sales tax, and excise tax. Each serves a specific purpose and impacts different aspects of daily life. For instance, state income tax is based on your earnings, while property tax affects homeowners. Sales tax applies to retail purchases, and excise tax targets specific goods and services.

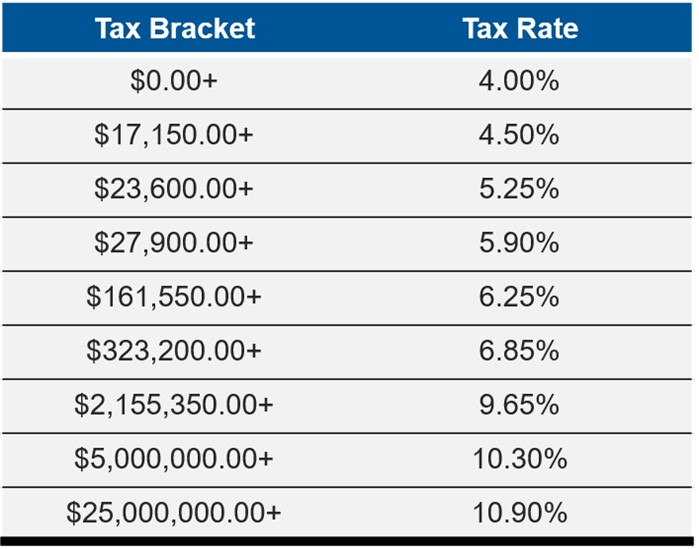

State income tax rates in New York vary depending on your income level. As of the latest updates, the state employs a progressive tax system, meaning higher earners pay a larger percentage of their income in taxes. This system aims to ensure that those with greater financial resources contribute more to the state's coffers. Additionally, New York offers various deductions and credits to help reduce your taxable income, such as the dependent care credit and the child tax credit.

Property taxes are another significant component of Taxes NY. They are calculated based on the assessed value of your property and are used to fund local services like schools and public safety. Homeowners should be aware of any changes in property assessments, as this can directly affect their tax bill. Similarly, sales tax impacts everyone who makes purchases in the state, with rates varying by county. Understanding these components and how they interact can help you better manage your tax responsibilities.

How Do State Income Taxes Work in New York?

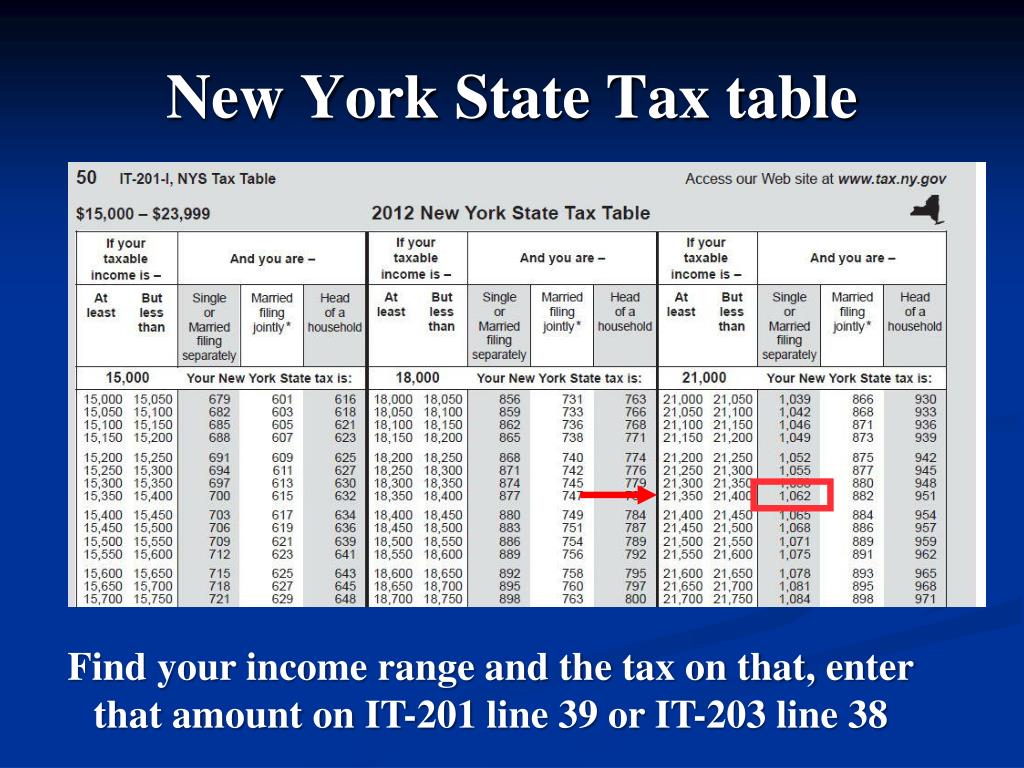

State income taxes in New York are a critical part of the state's revenue generation strategy. The tax system is designed to be fair and equitable, ensuring that all residents contribute according to their ability to pay. To calculate your state income tax, you'll need to determine your taxable income, which is your gross income minus any allowable deductions and exemptions. Once you have your taxable income, you can apply the appropriate tax rate based on your filing status.

For example, single filers with a taxable income below a certain threshold may pay a lower rate, while those earning more will fall into higher brackets. It's important to note that New York also offers a variety of tax credits that can further reduce your liability. These credits are designed to assist specific groups, such as low-income families, students, and the elderly. By taking advantage of these credits, you can significantly lower the amount of taxes you owe.

Furthermore, New York residents who work in other states may need to consider dual-state tax obligations. If you earn income in another state, you might be subject to that state's taxes as well. However, New York has reciprocity agreements with some states, allowing you to avoid double taxation. Understanding these nuances is crucial for anyone with out-of-state income sources.

Read also:Aubrey Plaza Husband

What Are the Property Tax Rates in New York?

Property taxes in New York are a major concern for homeowners, as they directly impact the cost of living. The rates vary by county and municipality, with some areas having significantly higher rates than others. Property taxes are calculated based on the assessed value of your property, which is determined by local assessors. This value can change annually, depending on factors like market conditions and property improvements.

Homeowners should be aware of the appeals process if they believe their property has been over-assessed. By challenging the assessment, you may be able to lower your tax bill. Additionally, New York offers several programs to help reduce property taxes for eligible residents. For instance, the STAR program provides exemptions for homeowners, while the Enhanced STAR program offers additional benefits for seniors. Understanding these programs and how to apply for them can help you save money on your property taxes.

Why Is It Important to Stay Compliant with Taxes NY?

Staying compliant with Taxes NY is crucial for avoiding penalties and maintaining financial stability. The state takes tax compliance seriously and imposes strict penalties for late filings, underpayments, and other violations. These penalties can quickly add up, leading to significant financial burdens for individuals and businesses alike. Therefore, it's essential to understand your obligations and meet all deadlines.

One of the best ways to ensure compliance is by keeping accurate records of your financial transactions throughout the year. This includes tracking income, expenses, and any tax-related documents. By maintaining organized records, you can easily prepare your tax returns and respond to any inquiries from the tax authorities. Additionally, staying informed about changes in tax laws and regulations can help you avoid common pitfalls and ensure you're meeting all requirements.

Another important aspect of compliance is understanding the various deadlines associated with Taxes NY. For example, state income tax returns are typically due by April 15th, while property tax payments may have different due dates depending on your location. Missing these deadlines can result in penalties and interest charges, so it's vital to mark them on your calendar and plan accordingly. By staying proactive and informed, you can ensure smooth and hassle-free tax compliance.

What Are the Penalties for Non-Compliance with Taxes NY?

Non-compliance with Taxes NY can lead to severe consequences, including financial penalties, legal action, and damage to your credit score. The state imposes penalties for late filings, underpayments, and failure to pay taxes altogether. These penalties can accumulate over time, making it increasingly difficult to get back on track. For instance, if you fail to file your state income tax return by the deadline, you may face a late filing penalty of 5% of the unpaid tax for each month the return is late, up to a maximum of 25%.

In addition to penalties, non-compliance can also result in interest charges on any unpaid taxes. The interest rate is determined by the state and is applied to the outstanding balance until it is fully paid. This can significantly increase the total amount you owe, making it even more challenging to resolve your tax issues. Furthermore, repeated non-compliance may lead to legal action, such as liens or levies on your assets, which can have long-lasting effects on your financial well-being.

How Can You Avoid Common Tax Mistakes in New York?

Avoiding common tax mistakes is essential for maintaining compliance and avoiding unnecessary complications. One of the most common mistakes is failing to report all sources of income. Whether it's from a side job, freelance work, or investments, all income must be reported to ensure accurate tax calculations. Another mistake is overlooking available deductions and credits, which can result in paying more taxes than necessary.

To avoid these pitfalls, consider using tax preparation software or consulting with a tax professional. These resources can help you identify all relevant deductions and credits, ensuring you're maximizing your savings. Additionally, staying informed about changes in tax laws and regulations can help you stay ahead of potential issues. By taking a proactive approach and being diligent in your tax planning, you can avoid costly mistakes and ensure smooth compliance with Taxes NY.

What Are the Available Deductions and Credits for Taxes NY?

Taxes NY offers a variety of deductions and credits to help reduce your tax liability and improve your financial situation. These benefits are designed to assist specific groups, such as low-income families, students, and the elderly. Understanding what deductions and credits are available and how to qualify for them is crucial for maximizing your savings.

Some of the most popular deductions include the standard deduction, itemized deductions, and education-related deductions. The standard deduction allows you to reduce your taxable income by a fixed amount, while itemized deductions let you claim specific expenses, such as mortgage interest or charitable contributions. Education-related deductions, such as the student loan interest deduction, can help ease the financial burden of paying for higher education.

In addition to deductions, New York offers several tax credits that can further reduce your liability. These include the dependent care credit, the child tax credit, and the earned income tax credit (EITC). Each credit has specific eligibility requirements, so it's important to review them carefully to determine if you qualify. By taking advantage of these deductions and credits, you can significantly lower the amount of taxes you owe and improve your overall financial health.

How Can You Minimize Your Taxes NY Liability?

Minimizing your Taxes NY liability involves strategic planning and taking full advantage of available deductions and credits. One effective strategy is to maximize your contributions to tax-advantaged accounts, such as retirement plans and health savings accounts (HSAs). These contributions can reduce your taxable income, lowering your overall tax burden. Additionally, investing in tax-efficient vehicles, like municipal bonds, can help you avoid paying taxes on certain types of income.

Another approach is to time your income and expenses strategically. For example, if you expect to be in a higher tax bracket next year, you might consider accelerating income into the current year to take advantage of lower rates. Conversely, if you anticipate being in a lower tax bracket next year, you might defer income to reduce your current year's tax liability. Similarly, timing your deductions and credits can help you optimize your tax savings.

What Are the Best Practices for Filing Taxes NY?

Following best practices when filing Taxes NY can help ensure a smooth and error-free process. Start by gathering all necessary documents, including W-2s, 1099s, and any other income or expense records. This will make it easier to accurately complete your tax return and avoid mistakes. Next, consider using tax preparation software or consulting with a tax professional to ensure you're taking full advantage of all available deductions and credits.

When filing your return, double-check all information for accuracy and completeness. This includes your Social Security number, income figures, and any deductions or credits you're claiming. Submitting an incomplete or inaccurate return can lead to delays and potential penalties. Finally, keep copies of all your tax documents and correspondence with the tax authorities in case you need to reference them in the future. By following these best practices, you can ensure a successful and stress-free tax filing experience.

FAQs About Taxes NY

What Are the Deadlines for Filing Taxes NY?

The deadline for filing state income tax returns in New York is typically April 15th. However, if this date falls on a weekend or holiday, the deadline may be extended to the next business day. It's important to note that property tax payments may have different due dates depending on your location, so be sure to check with your local tax authority for specific deadlines. Missing these deadlines can result in penalties and interest charges, so it's crucial to plan accordingly.

Can You File Taxes NY Online?

Yes, you can file your Taxes NY online through the New York State Department of Taxation and Finance's e-filing system. E-filing offers several advantages, including faster processing times, electronic acknowledgment of receipt, and direct deposit of any refunds. To e-file, you'll need to use tax preparation software that is approved by the state and submit your return electronically. This method is secure, convenient, and can save you time and effort compared to traditional paper filing.

What Should You Do If You Can't Pay Your Taxes NY on Time?

If you're unable to pay your Taxes NY on time, it's important to act quickly to minimize penalties and interest charges. First, file your tax return by the deadline, even if you can't pay the full amount owed. This will help you avoid late filing penalties. Next, contact the New York State Department of Taxation and Finance to discuss your situation and explore available payment options, such as installment agreements or offers in compromise. By taking proactive steps, you can work towards resolving your tax issues and getting back on track.

Conclusion

Taxes NY is a complex but essential aspect of life for residents of the Empire State. By understanding the various components of the state's tax system, staying compliant, and taking advantage of available deductions and credits, you can effectively manage your tax obligations and improve your financial well-being. Whether you're a homeowner, small business owner, or employee, the information provided in this article will empower you to make informed decisions and ensure you're maximizing your savings. Remember to stay informed about changes in tax laws and regulations, and don't hesitate to seek professional advice if needed. With the right knowledge and resources, you can navigate the world of Taxes NY with confidence and ease.